.png)

Conspiracy: Who Truly Benefits From the US-Iran War?

- A. Royden D'Souza

- Mar 30

- 20 min read

The US-Iran war erupts in the Middle East; the heart of global oil production. Iran closes the Strait of Hormuz, through which roughly 20% of the world’s daily oil consumption flows. Oil prices surge past $100, spiking toward $126 at the peak. The headlines scream about geopolitics, casualties, and diplomatic maneuvering.

But beneath the surface, a different story is playing out; one about money. While the public focuses on the conflict, a hidden financial architecture is quietly transferring wealth. The question is not just who wins the war, but who profits from it.

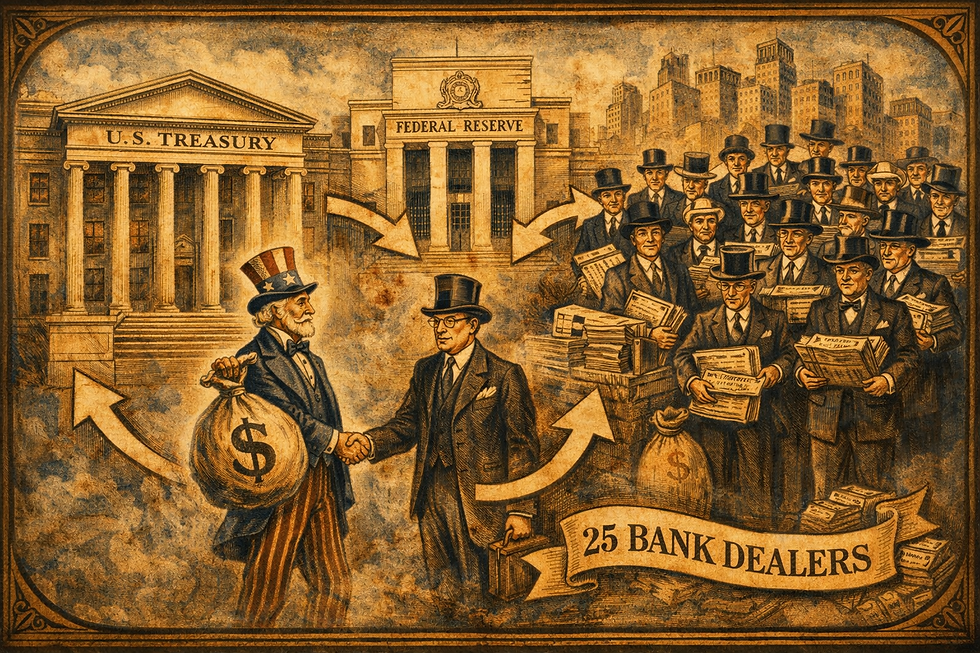

The Engine of US-Iran War: The Petrodollar Loop

The war’s financial impact begins with a simple mechanism: oil is priced in dollars.

When Iran chokes the Strait of Hormuz, oil prices spike. Foreign countries—especially major importers like Japan, South Korea, and European nations—suddenly need more dollars to pay for the same volume of oil. This surge in dollar demand pushes the US Dollar Index (DXY) higher—roughly 4% since the war began.

A stronger dollar gives the Federal Reserve room to keep interest rates high (or even raise them) without fearing a currency collapse. And high rates serve a dual purpose: they fight inflation (the official reason) and they generate massive risk‑free income for the banks (25 select banks linked to financial families) that sit at the Fed’s trading desk.

At the same time, oil‑exporting nations (Gulf nations), many of whose central banks and sovereign wealth funds are intertwined with the same financial families (Rothschild, Warburg, Schiff, etc.) receive massive dollar surpluses.

They recycle those petrodollars back into US Treasury bonds (they use those dollars to buy US Treasury bonds. The primary dealers (the select banks that transact directly with the Fed—the Banking Cabal) underwrite those bond sales, collect fees, and gain advance intelligence on capital flows.

The result is a self‑reinforcing loop: War → high oil → dollar demand surges → Fed hikes or holds rates → more dollar strength → foreign holders recycle petrodollars into US debt → the financial institutions that control the primary dealer system profit from underwriting, trading, and holding that debt.

Again, it's not the American commoners that benefit, but rather the banking interests (especially Wall Street) who have much to gain.

The Plumbing: How the Financial System Extracts Profit

To understand who benefits, we must look at the machinery; the same machinery that operates whether the market goes up or down.

Primary Dealers: The Exclusive Club

When the Fed injects liquidity (as it’s doing with $40 billion per month in T‑bill purchases), it does so exclusively through a select group of 25 primary dealers.

These are the only private institutions that sit at the Fed’s trading desk. The list includes J.P. Morgan Securities, Goldman Sachs & Co., Morgan Stanley & Co., Citigroup Global Markets, BofA Securities, Wells Fargo Securities, and others.

How they profit from the war:

1. T‑bill auctions and Fed purchases

The Treasury issues T‑bills to fund government operations. Primary dealers are mandated (a fake word to mask partiality toward select banks of the Banking Cabal) to bid in every auction.

If they cannot sell those T‑bills to other investors, they have a guaranteed buyer: the Federal Reserve (which was initially formed by this same Banking Cabal, although mainstream tries to hide this fact).

When the Fed buys the T-bills from these select banks, it credits their reserve accounts with electronically created money. Those reserves immediately start earning Interest on Reserve Balances (IORB); currently 3.65%. This is risk‑free income. On a $1 billion purchase, that’s $36.5 million per year for the select banks.

2. Interest on reserves

Even without lending, the banks collect billions annually just by parking reserves at the Fed. During the high‑rate period triggered by the war, this income stream swells. (Wall Street's pockets fill up)

3. Capital relief

In March 2026, the Fed rolled back "stricter capital requirements," freeing up an estimated $200 billion in excess capital for the six largest banks [JPMorgan (yes, the one accused of sinking the Titanic, which had all the bankers opposing the creation of the Federal Reserve/Fed), Goldman Sachs, Morgan Stanley, Citigroup, Bank of America, Wells Fargo].

This capital can be deployed into stock buybacks (returning cash to shareholders), lending (earning interest spreads), or trading activities; all while the banks continue to earn IORB on their reserves.

4. Standing repo and reverse repo facilities

The Fed offers dealers (25 select banks of the Banking Cabal) a Standing Overnight Reverse Repo Facility at 3.5%, a guaranteed floor for short‑term yields, and a repo facility that provides liquidity when needed, a safety net ordinary market participants do not have.

5. Treasury auction fees

As primary dealers, they earn underwriting fees and trading profits on every Treasury issuance. They sit at the front of the line.

6. Petrodollar recycling

They act as counterparties for foreign official accounts, collecting fees on every Treasury trade executed for foreign central banks and gaining intelligence on capital flows.

The Hidden Transfer: Fed Losses and the Taxpayer

When the Fed raised rates aggressively starting in 2022, its costs (interest paid to banks) skyrocketed while its income from older, lower‑yielding securities lagged.

By October 2024, cumulative losses of the Fed exceeded $200 billion. The Fed recorded these as a “deferred asset”—an IOU from itself. In reality, the IOU is a tax leash on future citizens of the US. In simple terms, the Fed is tying its debt load on the backs of future Americans.

During those loss years, remittances to the Treasury dropped from over $100 billion annually to near zero. The Treasury had to borrow that money elsewhere, increasing the national debt. Taxpayers ultimately service that debt.

The losses are not a direct tax, but they are a hidden transfer: from taxpayers to the banks that collected interest on their Fed reserves during the high‑rate period.

In simple terms, the Fed was prioritizing paying interests to the select banks of the Banking Cabal rather than funding the US Treasury (government), which meant the government had to borrow from somewhere else. Maybe issuing more T-Bills, so the dealers (Banking Cabal) can buy more of it and sell it at profit + interest to the Fed.

Now that rates are beginning to be cut, the deferred asset is slowly shrinking (which is necessary to prevent an uprising). They know there's a limit to looting citizens blind. But the damage is done: the public absorbed the cost while the banks booked the profits.

The Beneficiaries: Who’s Getting Rich

TIER 1: Central Bankers – The Big Winners

Central bankers spent 2024‑2025 in an uncomfortable spot: inflation cooling but not fast enough to justify aggressive rate cuts. The war solved their problem.

Oil‑driven inflation gave them a perfect excuse to keep rates high without taking the blame for slowing growth. Fed Chair Powell can now say rate cuts depend on inflation, and the war makes that impossible in the near term. The ECB faces the same dynamic, with markets now pricing multiple rate hikes.

The war gave them cover and an escape hatch: they can tighten without being blamed for the crisis. As Bloomberg’s Tom Orlik put it: “Central banks can set interest rates; they can’t reopen the Strait of Hormuz.”

Not to mention the main petrodollar reason, which we already covered.

TIER 2: The Military‑Industrial Complex

Defense contractors (Lockheed Martin, Raytheon, Northrop Grumman) benefit from surging arms sales, replenishment of munitions, and accelerated procurement of systems showcased in the conflict.

In a protracted “managed conflict,” they secure multi‑year contracts with cost‑plus pricing, ensuring guaranteed margins.

The same banks that underwrite Treasury debt also finance defense contractor working capital and sit on their boards through interlocking directorates. War guarantees predictable budget flows, and those flows are laundered through the primary dealer system.

TIER 3: The Silent Winners

Russia: As the US pressures Iran, global oil buyers scramble for alternatives. Washington has quietly relaxed sanctions enforcement to ease supply. Russia’s crude oil sales to India have jumped by 50% since the war began. Moscow could earn up to $5 billion more by the end of March alone, on track for its biggest year of fuel‑related revenues since 2022.

However, to ensure the prices remain high enough to maintain petrodollar supremacy and prevent non-dollar buying, the Wall Street is using its proxy in Ukraine to strike Russian oil refineries.

Norway: With Russian gas politically toxic (and getting attacked by Ukraine) and Middle East supplies disrupted, Norway, already wealthy from its sovereign oil fund, is ramping up production as Europe’s stable, trusted alternative.

Canada: Canada markets itself as a stable, reliable, values‑based energy producer. While it can’t ramp up overnight, protracted conflict makes its oil sands increasingly valuable.

Indonesia: As natural gas prices soar, some countries turn back to coal. Indonesia, a massive coal exporter, is seizing the opportunity as coal prices rise alongside oil.

US Oil Industry (with an asterisk): American shale producers make more per barrel. But many have physical operations in the Gulf region (ExxonMobil’s Qatar facility was hit by missiles), and years of capacity cuts limit rapid scaling. The gains are real but capped.

Again, these benefits are secondary results, and not primary drivers of the war. The primary reasons revolve around Wall Street and the petrodollar—like it's always been, since World War I (First Banker War).

The Losers: Who’s Getting Crushed

TIER 1: The Devastated

South Korea: Gets 70% of its crude oil from the Middle East. The Strait closure is existential for its industrial economy. Worse, South Korea makes more than half of the world’s memory chips; an energy‑intensive industry. High energy costs translate into lost competitiveness. The stock market has slumped; politicians warn openly of risk to the country’s most vital industry.

Sri Lanka, Bangladesh, Philippines: These fragile economies face fuel rationing, four‑day work weeks, and school closures. They have no buffers for $100+ oil.

Pakistan: Introduced “bill‑saving” measures; schools close, businesses shut early, people stay cold in winter. This is what an energy shock looks like in a country without fiscal space.

TIER 2: The Unexpectedly Exposed

United Kingdom and Europe: Europe relies on energy imports; the UK gets over half its energy from oil and gas. The Bank of England faces a classic stagflation trap: raise rates and worsen demand, or let inflation run hot. Markets have reversed expectations and now price rate hikes.

Japan: Imports more than 80% of its oil via the Strait. The yen is hovering near 160 to the dollar; a level that prompted intervention in 2024. The Bank of Japan faces a brutal choice: raise rates to defend the yen (harming growth) or keep rates low and accept higher import costs.

Gulf Producers (Saudi Arabia, Qatar, UAE): Iran isn’t attacking random tankers; it’s targeting America’s allies. Saudi and Qatari energy infrastructure has been hit. Qatar’s Ras Laffan industrial hub, one of the world’s largest LNG facilities, has been shut down and sustained missile damage.

These countries produce oil and gas, but they can’t sell what they can’t safely produce and ship. They’re losing market share to Russia, Norway, and Canada precisely because they’re on the front lines.

TIER 3: The American Household

President Trump said when oil goes up, America “makes a lot of money.” By “America,” he meant the aggregated balance sheet; the US is now a net oil exporter. But those dollars do not trickle evenly.

They concentrate in the hands of oil company shareholders (mostly, from the same Banking Cabal), executives, and most prominently, the financial institutions that underwrite, trade, and lend to the industry; the same primary dealers that earn risk‑free interest from the Fed.

For the American household, high oil prices mean something else: more expensive gasoline, higher heating bills, inflated prices for every good that depends on transportation. Americans are the world’s biggest per‑capita oil consumers.

The “nation” may book a net gain on paper, but the gain is captured by the financial and corporate elite, while the cost is deducted directly from the wallets of ordinary citizens.

The Families (Banking Cabal) & Their New Plantation

The Federal Reserve is technically a public institution, but not really. In simple terms, it's more like an hybrid institution that allows the Banking Cabal to dip into the nation's wealth.

The primary dealers that transact with the Fed are definitely private. And the families that built these banks—Morgan, Rothschild, Warburg, Schiff—have been central to global finance for centuries. Not to mention, they were key to creating the Fed.

Public ownership data shows Vanguard, BlackRock, and State Street as the largest shareholders of JPMorgan, Goldman Sachs, etc. But dynastic families rarely hold assets in their own names. They operate through a web of trusts, shell corporations, family offices, private foundations, and nominee accounts that do not appear in 13F filings.

A single family could control a 5% stake split across fifty entities—each registered to a law firm in Delaware, a trust in the Cayman Islands, or a foundation in Switzerland—without triggering disclosure thresholds. Vanguard itself is a pass‑through vehicle; if its underlying investors include opaque family trusts, the ultimate beneficial ownership becomes virtually untraceable.

The appearance of diffuse institutional ownership becomes the perfect camouflage for concentrated dynastic control.

The Ultimate Hedge: The Families’ Gold

If the families have been accumulating physical gold for centuries—through colonial plunder, central bank dealings, and control of the London Gold Fix—their holdings are immense.

Estimates range from 10,000 to 50,000+ tonnes. For perspective, total gold ever mined is ~216,000 tonnes; central banks hold ~35,000 tonnes. An aggressive estimate would mean the families (like Rothschild) hold more gold than all central banks combined.

This gold is the ultimate hedge. In a system‑break scenario—uncontrolled escalation, dollar collapse—it becomes the only true money, turning collapse into a windfall. The families lose control of the dollar‑debt‑yield machine, but they do not lose wealth.

They simply transition from invisible architects of a managed system to unassailable survivors holding the one asset everyone else will scramble for. Gold.

Three Scenarios: How the Machine Plays Out

Scenario A: Controlled De‑escalation (Short War)

What it looks like: A managed settlement that leaves the petrodollar system intact, Iran’s threat neutralized, Gulf monarchies re‑subordinated. Oil retreats to $70‑80.

Financial mechanism: The families’ banks and the Fed have already extracted maximum profit from the initial shock (high oil → dollar spike → petrodollar fees; high rates → IORB income; capital relief). Now they lock in gains. The Fed cuts rates gradually; not because inflation is beaten, but to repackage the narrative as “victory over war‑driven inflation.” Bond prices rise; dealers sell into strength. Gold rallies, but central bank selling (to themselves) caps it.

Who wins: Primary dealers book trading profits on the way down; Treasury refinances debt at lower rates; families time the exit perfectly.

Military‑industrial complex: Short war denies them sustained contracts. They get a spike, then a “peace dividend” hangover. Their institutional shareholders accept it as controlled profit extraction, but the MIC prefers longer conflict.

Who loses: Anyone who bought gold and sells before the controlled rally; Russia’s windfall ends (but they are bought off with sanctions relief).

Scenario B: Long “Managed” Conflict (Permanent War)

What it looks like: Strait partially closed for 12‑24 months; oil at $100‑120; rates high but not breaking the system; periodic escalations keep volatility alive.

Financial mechanism: This is the ideal state.

High oil = permanent petrodollar demand → foreign central banks buy dollars → recycled into Treasuries → primary dealers underwrite, collect fees, capture spreads.

Sustained high rates = permanent IORB income; the deferred asset grows, but that’s a future taxpayer burden; real cash flows to banks now.

Volatility = trading desk heaven (spreads, margin calls, repo fees).

Gold suppressed (artificially), preventing it from challenging the dollar.

Who wins: Banks earn steady risk‑free interest and fees; oil majors with hedging desks capture spreads; Treasury sees lower borrowing costs due to strong foreign demand.

Military‑industrial complex: Ideal environment—multi‑year IDIQ contracts, cost‑plus pricing, guaranteed margins. The MIC and financial families are symbiotic: war generates deficits that justify the financial architecture, and defense contractors are the visible tip.

Who loses: Middle class in importing nations; any attempt to break dollar hegemony is quietly sabotaged.

Scenario C: Uncontrolled Escalation (System Break)

What it looks like: Full‑scale regional war; oil spikes to $160+; inflation expectations unmoored; Fed forced to raise rates into recession, breaking the banking system.

Financial mechanism: The system’s nightmare.

Petrodollar recycling breaks as developing nations default on dollar debt; dollar’s reserve status faces a run.

Fed’s balance sheet breaks as interest paid to banks dwarfs income; deferred asset explodes.

Gold becomes the only safe haven as banks and institutions outside the Banking Cabal circle lose confidence in Dollar assets and buy physical, bypassing paper markets; a gold breakout above $5,000 signals dollar dominance is over.

Primary dealers face counterparty risk from derivatives; the Fed must choose between letting them fail or bailing them out in public view.

What Does “Counterparty Risk from Derivatives” Mean for Primary Dealers/Banks?

In simple terms: counterparty risk is the risk that the other party in a financial contract fails to fulfill its obligations. When that contract is a derivative—a financial instrument whose value is derived from something else (interest rates, oil prices, currencies, credit events)—the risk multiplies because derivatives are often leveraged, interconnected, and opaque.

1. Primary Dealers as Derivatives Hubs

The 25 primary dealers (Goldman Sachs, J.P. Morgan, etc.) are the largest dealers in over‑the‑counter (OTC) derivatives. They sit at the center of a web of contracts with:

Hedge funds – betting on oil prices, interest rates, currency moves.

Corporations – hedging fuel costs, foreign exchange exposure.

Foreign central banks – swapping dollars for other currencies, managing reserves.

Other banks – clearing and settling positions.

The Federal Reserve – via reverse repo and other facilities.

Each of these relationships carries counterparty risk.

2. Why Derivatives Amplify the Risk

Unlike a simple loan, derivatives are often:

Leveraged – small margin requirements control large notional exposures. A 5% move in oil can wipe out a hedge fund’s collateral, leaving the primary dealer with an unsecured loss.

Bilateral – many OTC derivatives are not cleared through a central clearinghouse. Losses flow directly from one counterparty to another.

Interconnected – one default can trigger margin calls across the system, creating a cascade.

Hard to value – in a crisis, pricing breaks down; dealers may not know their true exposure until a counterparty fails.

3. The Specific Scenario in the War Paper

The paper describes Scenario C: Uncontrolled Escalation—full‑scale regional war, oil spikes to $160+, inflation unmoored, the Fed forced to raise rates into a recession. In that environment:

Oil derivatives: Hedge funds and commodity trading firms that are short oil (or long volatility) face massive losses. They may default on margin calls to their prime brokers (the primary dealers).

Interest rate derivatives: As rates rise sharply, positions that bet on low rates blow up. The primary dealers that sold interest rate swaps or swaptions to those counterparties suddenly face counterparty failures.

Currency derivatives: A dollar spike (as described) could crush emerging market central banks that hold dollar‑denominated derivatives. If they fail to pay, the primary dealers on the other side take the loss.

Credit derivatives: If the chaos causes corporate defaults, credit default swap (CDS) contracts get triggered. The primary dealers that sold protection may find their protection sellers (other banks or hedge funds) unable to pay.

Primary dealers face counterparty risk from derivatives; the Fed must choose between letting them fail or bailing them out in public view.

4. Why This Is a “System Break” Event

The primary dealers are not just ordinary banks. They are the only institutions that transact directly with the Federal Reserve. If one or more of them become insolvent due to derivative counterparty defaults, the plumbing of the Treasury market, the repo market, and the Fed’s own operations would seize up.

The Fed would then face a choice:

Let them fail – causing a cascade of margin calls, frozen markets, and potentially a collapse of the dollar funding system.

Bail them out – but in a way that reveals the hidden architecture: the Fed’s emergency lending powers would be used to rescue the very institutions that profited from the war’s volatility.

In a “controlled” scenario, the Fed manages the volatility so that no counterparty fails. In an uncontrolled scenario, the derivatives web unravels, forcing a public bailout that exposes the system’s true beneficiaries.

5. The Deeper Pattern

Derivatives counterparty risk is the modern equivalent of the medieval banking network’s vulnerability to a single king’s default. The Templars held deposits and made loans to monarchs; when Philip IV defaulted (by arresting them), the network broke.

Today, the primary dealers’ counterparty risk is dispersed across thousands of contracts, but the structure is the same: a small, interconnected group of privileged institutions that lend, trade, and hedge with each other and with the central bank.

When the system is stressed, the central bank must choose between letting the privileged institutions fail—and taking down the whole financial system—or backstopping them in ways that make their hidden power visible.

That’s why “counterparty risk from derivatives” is the Achilles’ heel. It’s the mechanism through which an uncontrolled geopolitical shock could break the financial architecture that, in managed form, extracts profit from exactly those shocks.

Who wins: No one in the current power structure. This is a reset. New power centers emerge; those with physical assets (gold, energy, land) rather than paper claims.

Who loses: The public, whose pensions and savings are in dollars that hyperinflate; foreign holders of US debt; the middle class globally; the banks themselves; but the banking families (Banking Cabal) do not lose. Their hidden gold becomes the only true money, multiplying in real value. They lose control of the apparatus but not wealth.

Cold logic: This scenario will be prevented at almost any cost. The “experts” who talk about gold exploding as a bull case miss the point: the system will not allow a gold breakout that challenges dollar hegemony — as long as it's in their control to do so. They hold enough gold to fix its price... like how they do with diamonds by controlling its supply.

In a system‑break scenario—uncontrolled escalation, dollar collapse, cascading counterparty failures—the visible structures (corporations, banks, and ultimately the US state itself) would be consumed by the fire they helped ignite.

But for the banking families at the apex, destruction of the host nation is not destruction of wealth. Their true holdings—centuries of physical gold accumulated through Templar networks, colonial plunder, and central‑bank dealings—are not stored in American vaults alone.

They are distributed, portable, and sovereign unto themselves. When the British Empire reached its terminal phase after World War II, the same families quietly shifted the center of their operations from London to New York, shedding the husk of one imperial power and attaching themselves to the next.

The United States has served as the host body for dollar‑petrodollar extraction since Bretton Woods (a mechanism for transferring oil wealth to the banking families), but it is not the final host.

In a full collapse, the families would not fall; they would simply relocate the machine—gold intact—to whatever emerging power (or post‑American federation) proves capable of guaranteeing the security of their network. The nation burns; the network migrates.

A Second Front in the Profit Machine

While the Strait of Hormuz commands headlines, a quieter but equally potent supply shock is unfolding in the heart of Russia’s energy infrastructure. Since late 2025, Ukraine has launched a sustained wave of long‑range drone strikes against Russian oil refineries; targeting not just military assets but the very facilities that turn crude into diesel, gasoline, and naphtha.

By March 2026, an estimated 12–15% of Russia’s refining capacity has been knocked offline, with some plants operating at a fraction of their pre‑war output.

The mainstream explanation is straightforward: Ukraine is degrading Russia’s war machine by cutting off fuel for tanks, trucks, and aircraft. But the strategic timing—intensifying just as Iran closes the Strait—reveals a secondary, financial purpose.

Together, the two choke points create a coordinated supply squeeze that maximizes global oil prices, and with them, the dollar‑petrodollar loop that enriches the primary dealer system.

The Mechanics of the Squeeze

1. Refining capacity is the true bottleneck: Crude oil is useless without refining. When Ukrainian drones hit refineries, they do not merely reduce Russian fuel exports; they force global buyers to scramble for alternative refined products. Diesel prices, already elevated by Middle East tensions, jump another 8–10% within days of each major strike. This incremental spike acts like a second gear on top of the crude‑price surge from Hormuz.

2. Russia’s response tightens the market further: Facing domestic fuel shortages, Moscow imposes export restrictions on gasoline and diesel. European and Asian markets—already competing for Norwegian, Indian, and US Gulf Coast refined products—see supply vanish overnight. The result: crack spreads (the profit margin for turning crude into fuel) blow out to levels not seen since 2022. The primary dealers’ trading desks, which hold inventories and derivatives on refined products, capture these spreads directly.

3. A second petrodollar effect: Countries that previously bought Russian diesel—such as Brazil, Nigeria, and parts of the Mediterranean—now must source refined products priced in dollars from US Gulf Coast refiners, the Middle East, or India (which itself processes Russian crude). Every shift toward dollar‑denominated refined products reinforces the same dollar‑demand loop described earlier. The Federal Reserve’s trading desk sees no disruption; it only sees more dollar‑based trade flowing through the same correspondent banks.

Who Profits from the Refinery Bombing Campaign?

US Refiners and Exporters: American refiners along the Gulf Coast—Valero, Marathon, Phillips 66—operate at near‑max capacity, shipping diesel and gasoline to Europe, South America, and even parts of Asia that have been displaced from Russian supply. Their stock prices rally alongside crude. But the real beneficiaries are the financial arms of the same primary dealers: J.P. Morgan and Goldman Sachs are among the largest lenders to these refiners, structure their commodity hedges, and earn fees on every export‑financing letter of credit.

The “Friendshoring” Oil Trade: India, which quadrupled its Russian crude imports since 2022, now faces a problem: it can buy the crude, but its own refining capacity is stretched. The solution? Indian refiners process Russian crude into diesel and ship it to Europe—a transaction that still flows through dollar‑denominated trade finance arranged by Wall Street banks. The sanctions architecture, designed with carve‑outs for “energy security,” ensures that the dollars keep moving and the fees keep accruing.

Speculative Positioning on the Supply Shock: Hedge funds and commodity trading desks—many of which are either owned by or intimately linked to the primary dealers—had already built long positions in refined products before the drone campaign accelerated. The strikes provide a predictable, repeatable catalyst. Each new refinery attack is telegraphed in advance through intelligence leaks, giving the in‑the‑know desks time to add exposure. When the attack hits and prices jump, the gains are captured by those who sat on the same side of the trade.

The Military‑Industrial Complex, Again: Ukraine’s long‑range drone program is funded largely by US and European defense budgets. Raytheon, Lockheed Martin, and General Dynamics supply the components, guidance systems, and maintenance contracts. The same banks that underwrite Treasury debt also underwrite defense contractor bonds and sit on their boards. In this sense, the refinery campaign is a two‑for‑one profit center: it generates immediate trading profits on energy markets while ensuring steady, multi‑year defense procurement.

The Strategic Rationale: A “Managed” Escalation

Why would Washington, which officially seeks to avoid $100+ oil, tacitly support strikes that lift prices? The answer lies in the same logic that governs the Hormuz closure: the political costs of high oil are distributed (American voters pay at the pump), but the financial benefits are concentrated (primary dealers, oil majors, defense contractors).

For the institutions that control the money supply, a modest, prolonged oil spike is preferable to either a quick resolution or a catastrophic blow‑up.

The refinery campaign offers “plausible deniability.” Ukraine claims it as a sovereign act of self‑defense. The US can publicly caution against strikes on energy infrastructure while privately continuing intelligence sharing and weapons supply.

Meanwhile, the market absorbs a series of small, repeated shocks rather than a single, panic‑inducing event. This is the hallmark of a managed conflict—volatility high enough to generate trading and fee income, but controlled enough to avoid systemic collapse.

Integration with the Three Scenarios

Scenario A (Short War): If peace talks suddenly succeed, the refinery campaign would be scaled back. But the physical damage to Russian refineries is not easily reversed; many require months or years to repair. Even a short war leaves a lasting refining deficit, keeping product prices elevated and sustaining the profit loop.

Scenario B (Managed Conflict): This is the natural habitat of the refinery strategy. Periodic strikes can be calibrated to maintain a price floor without provoking an all‑out escalation. Each strike serves as a “profit event” for traders and defense contractors, timed to coincide with Treasury auctions or Fed policy meetings to maximize market impact.

Scenario C (Uncontrolled Escalation): If Russia retaliates by attacking European energy infrastructure or widening the war, the refinery campaign could trigger the very system‑break scenario the families wish to avoid. Hence, the campaign is conducted with enough restraint to keep escalation in check; a tacit understanding between Washington and Moscow that attacking each other’s energy assets has limits.

The Bottom Line

Ukraine’s refinery campaign is not an accidental side effect of the war; it is a parallel financial instrument. By selectively destroying Russia’s ability to turn crude into fuel, it tightens global refined‑product markets, widens crack spreads, and forces more trade through dollar‑denominated channels; all while funding the military‑industrial complex and rewarding the trading desks of the primary dealers.

The strikes are announced with enough predictability to be front‑run by insiders, yet presented to the public as tactical battlefield necessities. Like the Strait of Hormuz closure, they are a lever in the larger machine; one that extracts wealth from the many and concentrates it among the few who sit at the center of the financial architecture.

Conclusion: The War as an Instrument

The Iran war is not a cause but an instrument. Its duration and intensity are calibrated to serve the financial interests mapped above; not the geopolitical talking points. The bankers on Wall Street profit not from a flat line but from the spike—in both directions.

At the outbreak, they front‑run the oil and dollar surge, positioning long on petrodollar fees and short on gold. As prices rocket, their banks collect risk‑free interest, their trading desks capture spreads, and their asset arms sell gold futures to the public while physically accumulating at suppressed prices.

When the narrative shifts, they orchestrate the controlled collapse: rate cuts, bond rallies, selling into strength. Every spike, up or down, transfers wealth from those who react to those who move first.

The surface narrative—peace talks, ceasefires, diplomacy—is puppetry. The real decisions are made by the same institutions that control the money supply, the primary dealer system, and the Fed’s balance sheet.

The “short war” scenario is what the system will try to sell you. The “managed conflict” scenario is the one that extracts maximum profit. The “uncontrolled escalation” is the one that would break the system, so it will be avoided—even if it means sacrificing the nominal objectives of the war.

Whenever an event appears inexplicable—a war that serves no clear national interest, a policy that seems self‑destructive, a catastrophe that brings only death and chaos—look not for strategic logic or human folly. Look for the transfer of wealth. Track the money.

Who is being paid? Who is being bailed out? Who is accumulating assets while others burn? The surface story will confuse; the shadows behind it will not. In every apparently irrational destruction, there is a silent creditor counting his profit. That is the fingerprint of the machine.

Comments